INDIA’S PASSIVE FPI OUTFLOWS MAY SOON BOTTOM AS USDINR NEARS 88-89

Summary

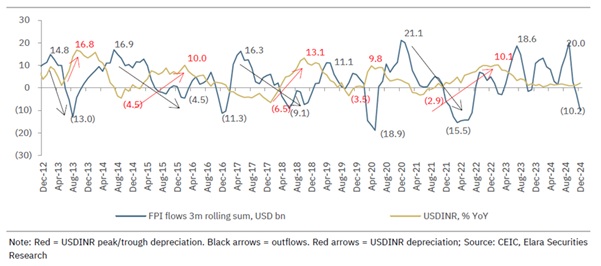

Passive Foreign Portfolio Investment (“FPI”) outflows from India may soon turn as USDINR moves towards 88-89. Historical trends show a median depreciation of 6.6% in trough-to-peak cycles over the last decade, with an average of 7.9%. If this pattern holds, the rupee could reach 88-89 by Q1 FY26, possibly reversing passive FPI outflows.

Historical patterns indicate that major depreciations in USDINR tend to follow phases of appreciation. The most notable depreciation in recent history occurred during the 2013-14 Taper Tantrum when the currency fell by ~16% within 3-4 months after FPI flows peaked at $14.8 billion. A similar decline was seen in 2018 due to trade war concerns, a 100-bps Fed rate hike, and domestic uncertainties linked to GST implementation, resulting in $25 billion in FPI outflows.

Given past trends, if current factors affecting the exchange rate persist, USDINR could rise to 88-89 by April-May FY26 based on median bottom-to-peak moves observed in previous years.

Cycles of USDINR and FPI flows show average peak depreciation of 8.3%

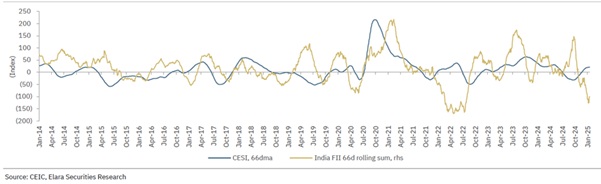

The US Economy and FPI Inflows: A Surprising Correlation

Contrary to common belief, a stronger U.S. economy does not necessarily drive capital outflows from India. Analysis of the Citi U.S. Economic Surprise Index (CESI) and India’s net FII equity flows since 2014 suggests a 25% positive correlation. Additionally, econometric modeling indicates that a 1% positive surprise in U.S. economic data has historically driven an inflow of approximately $82 million into Indian equities, with a lag of around one month.

Growth Surprises in the US are Generally Positive for India Flows

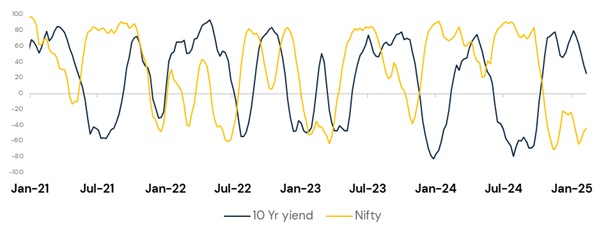

Correlation between US 10-Year Bond Yields and Indian (or Emerging) Markets

Historical data suggests a strong inverse correlation between U.S. 10-year bond yields and emerging market equities, including India. These asset classes often move in opposite directions, with rising U.S. bond yields drawing capital away from riskier markets. When the U.S. 10-year yield exceeds 4.3% to 4.4%, it often marks an inflection point where investors reallocate funds into U.S. bonds.

In September 2024, the U.S. 10-year yield was at 3.6%, but it has since risen to 4.6%. This surge has coincided with significant capital flows into U.S. assets, strengthening the dollar and contributing to large-scale FII outflows from India. A 4.5% risk-free return in U.S. dollars presents an attractive alternative, particularly as emerging markets continue to trade at elevated valuations.

Source: Vasuki Research

Conclusion: Volatility Ahead, but Structural Strength Remains

Although short-term market conditions remain uncertain, India’s long-term fundamentals continue to provide a solid foundation. Fiscal consolidation efforts, steady forex reserves, and resilient domestic flows support economic stability. While USDINR may weaken to 88-89, the expected reversal in passive FPI flows will be a critical development for investors tracking the evolving macroeconomic environment.

For more information, reach out to us at research@vasukiindia.com.

Disclaimer

This article is published for informational purposes only and does not constitute investment advice or analysis. The information presented has been sourced from public domains and has not been independently verified.

Vasuki Group makes no representations or warranties regarding the accuracy, completeness, timeliness, or reliability of the content. Neither Vasuki Group nor its affiliates, directors, employees, or representatives shall be liable for any errors, omissions, or reliance on the information provided.

This article does not constitute an offer, solicitation, or recommendation for any investment, securities transaction, or contractual engagement. Readers should conduct their own due diligence before making any financial decisions.

Any views expressed are those of the author and do not necessarily reflect the opinions of Vasuki Group. Further, Vasuki Group may hold or take positions in the market that differ from the views expressed in this article.

All rights reserved. Vasuki Group reserves the right to update or modify this article at its discretion.